On Could 28, Aave Labs introduced that its UK subsidiaries Push Labs Ltd. and Push Digital Belongings Ltd. acquired FCA registration as cryptoasset change suppliers, layered on high of the group’s present Digital Cash Establishment authorization.

Mixed with the MiCAR CASP license that Push Digital Belongings Eire Restricted secured from the Central Financial institution of Eire in November 2025, Aave now operates underneath a dual-permission framework masking each the UK and the EEA.

The licensing stack clears the trail for zero-fee fiat-to-stablecoin on and off-ramps and, in line with Stani Kulechov, “next-generation, zero-fee on-chain client monetary merchandise.”

Aave’s aggressive edge comes from its place because the largest on-chain credit score market, with practically $14 billion in whole worth locked (TVL) and $10.7 billion in excellent borrowings, in line with DefiLlama.

Including a regulated client funds layer to that stack would appear to be a random enlargement, until it feeds instantly into Aave’s lending protocol, which is precisely what Push is designed to do.

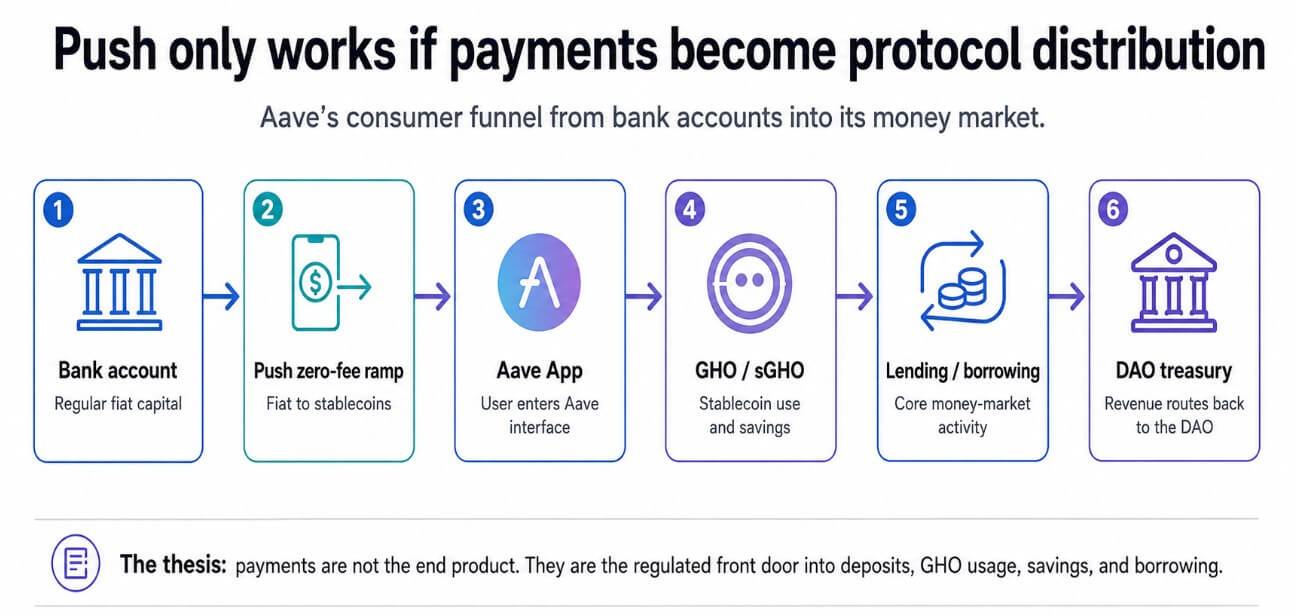

What makes Push value analyzing extra intently is that it’s being constructed because the regulated entrance door to Aave’s lending protocol, the channel by way of which financial institution accounts convert to stablecoins and stablecoins move into GHO, financial savings, and borrowing on Aave.

Why funds have traditionally failed Aave

Marc Zeller’s February governance audit tallied Aave Labs’ whole capitalization at roughly $86 million, with $16.2 million from the 2017 EthLend ICO, $32.5 million from enterprise rounds, $31.9 million in direct DAO funds, and roughly $5.5 million in swap charges he characterised as unapproved.

His framework utilized three inquiries to that determine: what did Labs ship, what did it value, and what was the return?

The audit concluded that non-core merchandise had not proven cost-per-outcome self-discipline commensurate with that funding. Zeller particularly known as out Horizon, Aave’s RWA market, for a spending-to-revenue ratio of roughly 24:1.

The broader indictment was that Labs had captured brand-adjacent income streams, akin to swap charges routed to a Labs-controlled pockets fairly than the DAO treasury, whereas increasing its product scope with no measurable influence on the protocol.

That critique formed the AIP 469 vote, which handed with roughly 75% of taking part tokens. It established the “Aave Will Win” framework, consisting of routing to the DAO treasury 100% of income from all Aave-branded merchandise, together with the frontend app, Aave Card, Aave Professional, swaps, and future client merchandise.

In change, Aave Labs acquired a $25 million stablecoin grant and 75,000 AAVE vesting over 48 months.

Zeller’s Aave Chan Initiative solid 166,200 tokens in opposition to, the most important single dissenting vote, earlier than asserting ACI would wind down totally by July.

| Merchandise | Determine / element | Why it issues |

|---|---|---|

| 2017 EthLend ICO | $16.2M | Early capitalization base |

| Enterprise rounds | $32.5M | Non-public funding behind Labs development |

| Direct DAO funds | $31.9M | DAO-funded product accountability |

| Swap charges characterised as unapproved | ~$5.5M | Core dispute over worth seize |

| Complete cited by Zeller | ~$86M | Baseline for “what did Labs ship?” critique |

| Aave Will Win funding | $25M + 75,000 AAVE | New check: funding tied to DAO income routing |

| Product-revenue routing | 100% to DAO treasury | Why Push is judged in a different way from prior facet quests |

The governance combat modified the accountability construction for non-core product growth, instantly shaping Push’s trajectory.

Labs can not seize payments-adjacent income independently, and any move Push generates falls underneath the DAO income framework. That strikes the motivation construction from “Labs builds a client fintech” to “Labs builds a distribution layer whose industrial output belongs to AAVE holders.”

Funds as a funnel and lending because the enterprise

Kulechov’s January framework submit confirmed that the majority Aave lending continues to be concentrated round ETH, BTC, and leverage-driven looping methods tied to crypto market cycles.

GHO’s circulating provide sits close to 584 million tokens, making it pale compared to USDT’s share of the $188 billion stablecoin market and USDC’s $76 billion.

Aave’s addressable stablecoin alternative is orders of magnitude bigger than its present penetration, and the disconnect comes all the way down to getting common capital into the protocol with out routing it by way of crypto-native infrastructure.

Aave already generates over $633 million in annualized charges and $81 million in annualized income. The lacking layer is a regulated, zero-fee ramp from financial institution accounts to stablecoins, and Push is constructed to provide it.

The person journey Push allows runs from a checking account to a zero-fee stablecoin ramp to the Aave App to GHO or sGHO financial savings to lending and borrowing. A generic funds product monetizes by way of spreads, interchange, or subscription charges.

Push’s income comes from customers transferring deeper into Aave’s cash market, depositing stablecoins, minting GHO, holding sGHO, and borrowing in opposition to collateral. The deeper customers go, the extra protocol income accrues to the DAO.

The Irish MiCAR license already helps zero-fee euro-to-stablecoin conversion, and the UK FCA registrations prolong that infrastructure to a second main regulated market, with EEA passporting rights already in place from Eire.

Coinbase, MoonPay, Ramp, and Revolut all compete for a similar fiat-to-crypto conversion move, and that market is inherently low-margin.

Push’s structural benefit lies in its non-custodial design, mixed with a regulated presence in two main markets, which removes one of the friction-heavy steps in changing an everyday client into an Aave depositor.

If Push retains even 2.5% of its transformed stablecoin move into Aave deposits, roughly $500 million at scale, it reaches parity with GHO’s present market cap. It creates an acquisition channel that operates totally outdoors crypto-native leverage cycles.

What has to carry

The bear case is equivalent to each prior Aave enlargement Zeller warned about, consisting of Push turning into a regulated funds layer with excessive ramp quantity and low protocol conversion.

If Push customers convert fiat to stablecoins and withdraw to exterior wallets or competing platforms, Push turns into costly infrastructure producing no Aave-native worth.

The FCA and MiCAR licenses allow authorized operation, and changing that permission into deposit development requires a client product that pulls customers away from Revolut, Monzo, and Coinbase on product high quality.

Revolut, Monzo, and Coinbase’s UK entity have occupied this marketplace for years with established compliance capabilities, model recognition, and built-in product suites.

The UK’s broader crypto licensing regime additionally introduces timing threat, because the FCA has confirmed that present Cash Laundering Regulation registrations is not going to mechanically convert into authorization underneath the forthcoming FSMA-based framework, set to take impact in October 2027.

Push’s present registration clears the trail for launch however doesn’t assure a frictionless transition into the stricter regime.

And the governance construction that makes Push’s income alignment credible depends upon Aave Labs sustaining sufficient inside cohesion to execute a client product roadmap.

Aave’s cash market is deep sufficient that Push solely has to maneuver a fraction of client stablecoin move into Aave deposits to justify its existence.

| State of affairs | What occurs | Key metric | Article implication |

|---|---|---|---|

| Bull case: money-market funnel | Push customers convert fiat, then retain funds in Aave deposits, GHO, or sGHO | Deposit retention, GHO provide development, sGHO adoption | Funds strengthens Aave’s lending moat |

| Base case: helpful ramp | Push will get adoption, however a lot of the move exits to exterior wallets or venues | Ramp quantity vs Aave deposit conversion | Useful infrastructure, however not a core development engine |

| Bear case: facet quest returns | Excessive compliance/product value, weak protocol conversion | Price per retained greenback, protocol income uplift | Zeller’s critique is validated |

| Regulatory threat case | UK FSMA transition or EEA compliance limits product design | Approval standing, launch scope, product restrictions | Licensing win turns into execution threat |

| Governance threat case | DAO/Labs alignment frays over prices, income, or product scope | DAO income share, reporting cadence, renewal votes | AWW framework faces its first main stress check |

If it does, funds grow to be Aave’s most essential acquisition channel, and Zeller’s cost-per-outcome framework lastly will get a product that passes it.

If Push produces ramp quantity with out protocol conversion, the framework applies in reverse: one other product layer, one other governance combat, the identical unresolved query about what Aave Labs builds that really strengthens the cash market versus what it builds for different causes.

The Aave Will Win framework was designed to make that distinction testable, and Push is the primary product that runs the experiment in a regulated client market.

{kind=link}