Hut 8 is pushing even additional into AI infrastructure than most different Bitcoin miners are. Its newest disclosures present an organization utilizing energy entry, knowledge heart leases, mission debt, and BTC-backed liquidity to construct the financing stack for that transfer.

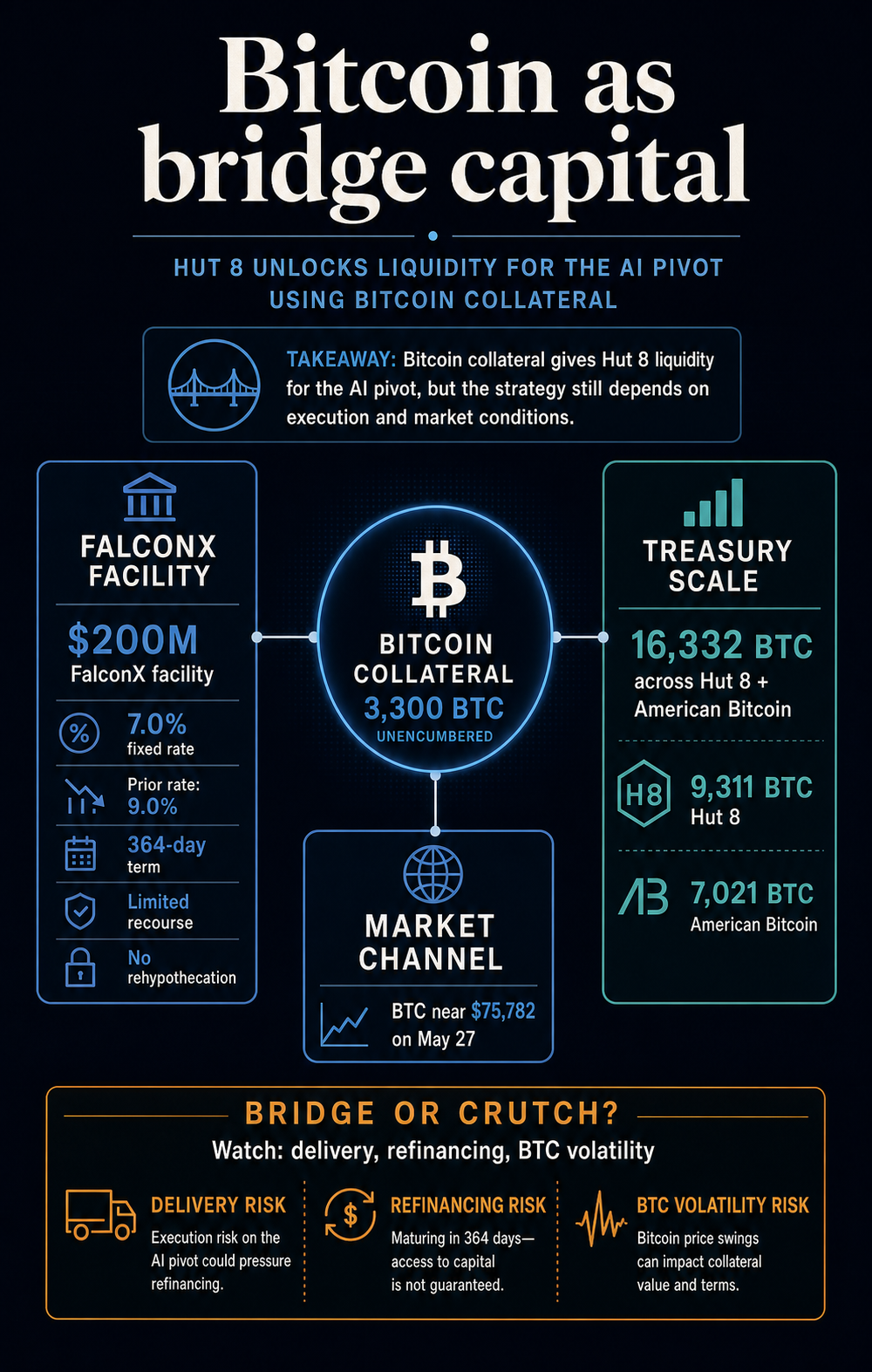

The corporate’s newest disclosures put numbers round that transition. Hut 8 reported $16.8 billion in triple-net, take-or-pay contracted lease income throughout two hyperscale AI campuses, then individually refinanced a $200 million Bitcoin-backed credit score facility with FalconX.

The brand new facility reduce the mounted price to 7.0% from 9.0% and unencumbered roughly 3,300 BTC from the prior collateral package deal.

Taken collectively, the disclosures present a miner id becoming one thing nearer to an infrastructure landlord. Hut 8 is popping megawatts, lease commitments, mission debt, and Bitcoin holdings into the equipment for a enterprise that relies upon much less on mining alone.

The result’s a case examine with extra substance than a generic AI pivot. Hut 8 is displaying a funded path into knowledge heart infrastructure, although the mannequin nonetheless wants working proof. The check is whether or not contracted AI money flows arrive on schedule and change into sturdy sufficient that Bitcoin collateral turns into a bridge as an alternative of a recurring supply of balance-sheet dependence.

The lease base turns energy into finance

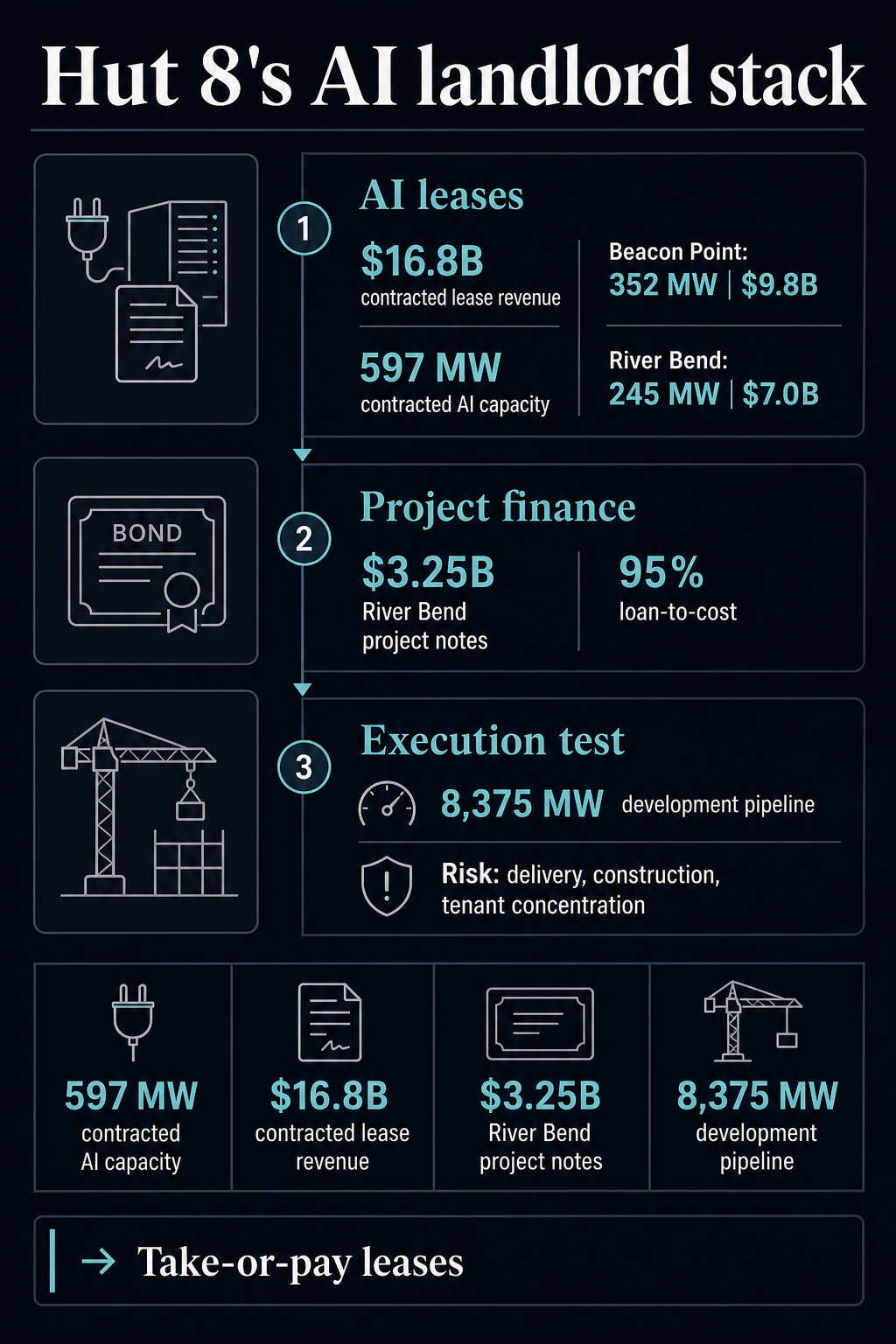

The strongest quantity in Hut 8’s first-quarter disclosure sits outdoors the Q1 revenue assertion: $16.8 billion of contracted lease income throughout River Bend and Beacon Level, protecting 597 MW of AI knowledge heart capability.

Hut 8 generated $71 million of income within the first quarter, together with $66 million from Compute, and posted a $253 million internet loss that included $295 million of primarily unrealized digital-asset losses.

The $16.8 billion determine represents long-term contracted lease worth that Hut 8 is presenting as the inspiration for a special type of enterprise.

The items are particular. Hut 8’s Beacon Level lease added 352 MW of IT capability and $9.8 billion of base-term worth. Its earlier River Bend lease added 245 MW and $7 billion of base-term worth, with Google offering a monetary backstop for the bottom lease time period.

Hut 8 is commercializing scarce energy and knowledge heart capability beneath long-term lease constructions. The attraction comes from contracts and energy entry quite than a token, a cloud slogan, or a imprecise compute promise.

Triple-net and take-or-pay phrases are designed to make these money flows extra financeable as a result of the tenant obligation is much less tied to day-to-day mining economics.

Hut 8’s disclosures line up throughout 4 transferring elements:

| Mannequin element | Hut 8 proof | Reader influence | Threat nonetheless dwell |

|---|---|---|---|

| Energy and websites | 597 MW of contracted AI knowledge heart capability throughout two campuses | Turns miner infrastructure into leaseable digital infrastructure | Supply, interconnection, development, and tenant focus |

| Contracted demand | $16.8 billion in base-term contracted lease income | Creates a financing story past hashprice publicity | Lease worth depends upon execution over lengthy timelines |

| Venture finance | $3.25 billion River Bend notes, non-recourse to Hut 8 | Reduces the necessity to fund all progress from fairness or BTC gross sales | Giant initiatives nonetheless carry price, schedule, and market dangers |

| Bitcoin steadiness sheet | $200 million FalconX BTC-backed facility and three,300 BTC unencumbered | Provides liquidity with out instantly promoting cash | Collateral worth nonetheless strikes with BTC |

Hut 8’s AI transition has extra to it than most, however every element nonetheless carries a special type of threat.

The leases cut back some income uncertainty. The bond financing reduces some parent-level funding strain. The Bitcoin facility improves liquidity. Nonetheless, all three depart Hut 8 with the duty of constructing, delivering, and working infrastructure for patrons whose necessities differ from Bitcoin mining.

Bitcoin turns into bridge capital

The FalconX refinancing is the clearest signal that Bitcoin is turning into a part of the financing equipment quite than solely the asset being mined.

The total Hut 8 launch distributed by means of Nasdaq described the power as a 364-day Bitcoin-backed mortgage with restricted recourse to pledged BTC, a no-rehypothecation covenant, mounted loan-to-value thresholds, and no loan-to-value ratchet triggered by declines in Bitcoin’s worth.

These phrases blunt a part of the plain criticism. The deal improves the phrases of a miner’s coin-backed borrowing as an alternative of worsening them to chase a brand new market.

Hut 8 lowered its mounted price of debt by 200 foundation factors and elevated Bitcoin held outdoors collateral covenants. The discharge valued the newly unencumbered cash at roughly $260 million as of Might 1, 2026, giving Hut 8 extra balance-sheet room with out promoting the asset.

That makes the power a greater instrument, however not a risk-free one.

Hut 8’s personal steadiness sheet reveals why the excellence is vital. Its 10-Q mentioned the corporate held about 16,332 BTC as of March 31, 2026, together with about 9,311 BTC held by Hut 8 and about 7,021 BTC held by American Bitcoin.

The combination truthful worth was about $1.11 billion, primarily based on roughly $68,222 per BTC. The identical submitting tied the first-quarter digital-asset loss to Bitcoin’s decline through the interval.

Immediately, Bitcoin trades close to $75,782 on CryptoSlate’s worth web page, down 2.1% over 24 hours and roughly 40% under its October 2025 all-time excessive. The market-price channel is the related threat.

Bitcoin can present liquidity and not using a sale, however the borrowing worth, covenant consolation, and refinancing backdrop nonetheless depend upon the asset’s market habits.

That’s the reason the AI landlord technique can’t be separated from the Bitcoin treasury technique. If AI leases produce dependable money flows, BTC collateral might be transitional capital. If supply slips, financing markets tighten, or Bitcoin weakens on the unsuitable time, the identical collateral can hold the pivot tied to the volatility it was meant to flee.

The miner label is turning into much less helpful

Earlier protection of miners’ AI pivot confirmed the broader id break up going through the sector. Miners are transferring towards AI and high-performance computing as a result of energy entry, cooling infrastructure, land, interconnection work, and industrial operations might be price extra beneath contracted greenback income than beneath compressed mining margins.

Hut 8 suits that broader sector shift. Public miners constructed companies round changing energy into BTC, and AI knowledge heart demand is now giving a few of them a second doable use for a similar bodily footprint.

The distinction is that AI prospects don’t purchase the identical factor the Bitcoin community buys. Mining can tolerate interruption when economics or grid situations change. AI tenants need uptime, supply certainty, dense energy, cooling, community structure, and creditworthy execution.

A miner with megawatts nonetheless has to change into a hyperscale landlord. It has to show an influence place into infrastructure that lenders and tenants will deal with as reliable.

Hut 8’s disclosures present each side of that transition. The corporate describes itself as an vitality infrastructure platform integrating energy, digital infrastructure, and compute. It additionally nonetheless stories digital-asset losses, BTC holdings, and publicity to mining economics.

Some Compute income and BTC holdings are held by American Bitcoin, a consolidated subsidiary, making Hut 8’s technique much less easy than a clear exit from mining.

That complexity is a part of the shift. The market is watching whether or not miners can cease being pure BTC proxies with out dropping the balance-sheet optionality that made their treasuries precious within the first place.

The strongest argument in Hut 8’s favor is that the AI pivot makes use of greater than Bitcoin-backed debt. The corporate mentioned it closed $3.25 billion of absolutely amortizing 16.5-year investment-grade senior secured notes to finance River Bend.

Hut 8 described the financing as non-dilutive and non-recourse to Hut 8, with loan-to-cost rising to about 95%.

That weakens the crutch argument. If project-level debt funds the campus and long-term leases assist the debt, then Bitcoin collateral is one a part of the construction quite than the entire. It’s a liquidity instrument alongside mission finance and contracted income.

The warning is that the monetary construction nonetheless has to change into operationally sound. River Bend continues to be advancing towards supply, Beacon Level nonetheless must be constructed out, and the corporate nonetheless has to transform an 8,375 MW growth pipeline into actual contracted capability.

Hut 8 additionally warned buyers about dangers tied to knowledge heart development, financing, energy growth, allowing, provide chains, technical challenges, and market situations.

Hut 8 is displaying that miners can finance a route into AI infrastructure once they have scarce energy, credible tenants, project-finance entry, and a Bitcoin steadiness sheet lenders will underwrite. It has but to indicate that the route is self-sustaining.

The following check is whether or not AI infrastructure money flows change into robust sufficient to push Bitcoin collateral into the background. In the event that they do, Hut 8’s BTC-backed financing will appear like bridge capital for a miner that efficiently monetized its energy footprint.

In the event that they fail to take action, the pivot will stay tethered to the identical balance-sheet asset that made the technique doable within the first place.

{kind=link}