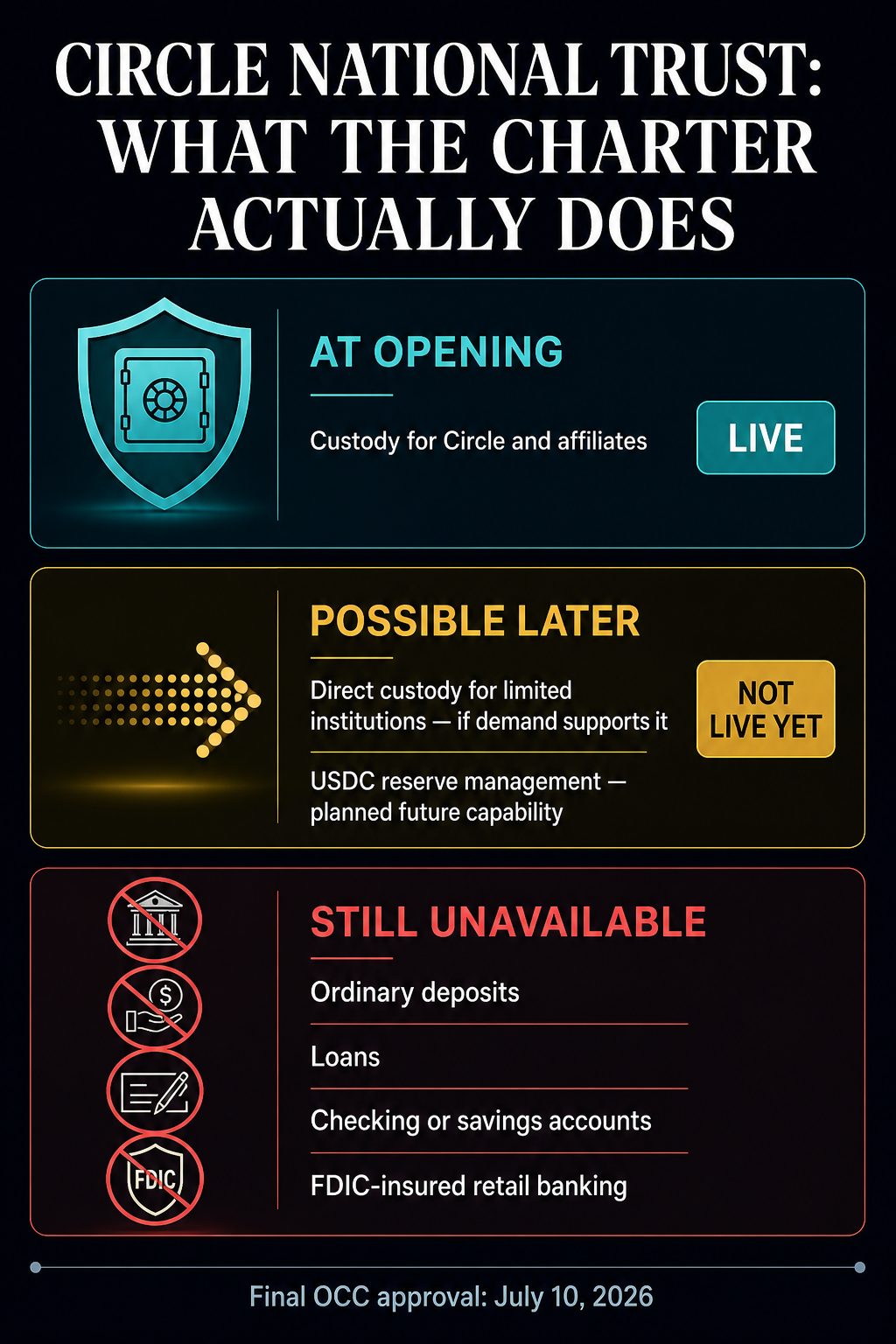

Circle acquired approval from the OCC on July 10 to determine a financial institution known as Circle Nationwide Belief. That doesn’t give the USDC issuer the powers most individuals affiliate with a industrial financial institution.

The nationwide belief financial institution can not settle for unusual deposits, make loans, provide checking or financial savings accounts, or present FDIC-insured retail banking providers. The choice is ultimate, not like the OCC’s preliminary conditional approval from December 2025, however its permitted enterprise stays centered on fiduciary custody.

What Circle can do at opening

Circle mentioned the financial institution’s authorized title shall be First Nationwide Digital Forex Financial institution, N.A., working as Circle Nationwide Belief. Upon opening, it is going to present fiduciary digital-asset custody for Circle and its associates underneath direct OCC supervision.

That’s the solely service Circle has confirmed for the financial institution’s opening. Circle mentioned the financial institution might finally present custody on to a restricted variety of establishments, specializing in banks and different regulated monetary organizations, if demand warrants growth.

Managing the USDC reserve can also be a future functionality somewhat than a service that arrives with the constitution. Circle has not disclosed when the financial institution will open or what extra operational steps should happen earlier than reserve administration strikes inside it.

The constitution’s strategic worth lies in larger management over the infrastructure supporting a stablecoin with a market capitalization of about $73.3 billion.

A federal constitution would let Circle deliver custody, and presumably reserve administration, underneath one roof as an alternative of relying as closely on exterior corporations. The corporate has not mentioned what which may save or whether or not it plans to alter its present companions.

The constitution offers Circle a federal fiduciary framework that competing stablecoin issuers might discover tough to match shortly. That might assist when banks and different regulated corporations determine which digital-dollar infrastructure they’re prepared to make use of.

It doesn’t mechanically deepen USDC liquidity or place the token in additional wallets, exchanges and fee merchandise. These distribution benefits stay contested as Open USD recruits main companions and challenges Circle’s issuer-led economics.

The constitution additionally carries political friction. The Unbiased Group Bankers of America argued through the utility course of that nationwide belief charters can present nonbank fintechs with bank-like advantages with out the complete capital and consumer-protection framework that applies to insured industrial banks. The OCC nonetheless granted ultimate approval.

The following checks are operational: when Circle Nationwide Belief opens, whether or not exterior establishments demand its custody service, and whether or not USDC reserve administration is later introduced underneath the belief financial institution. Till then, Circle has gained federal supervision for custody—not the deposit-taking and lending powers implied by saying it merely “grew to become a financial institution.”

{kind=link}