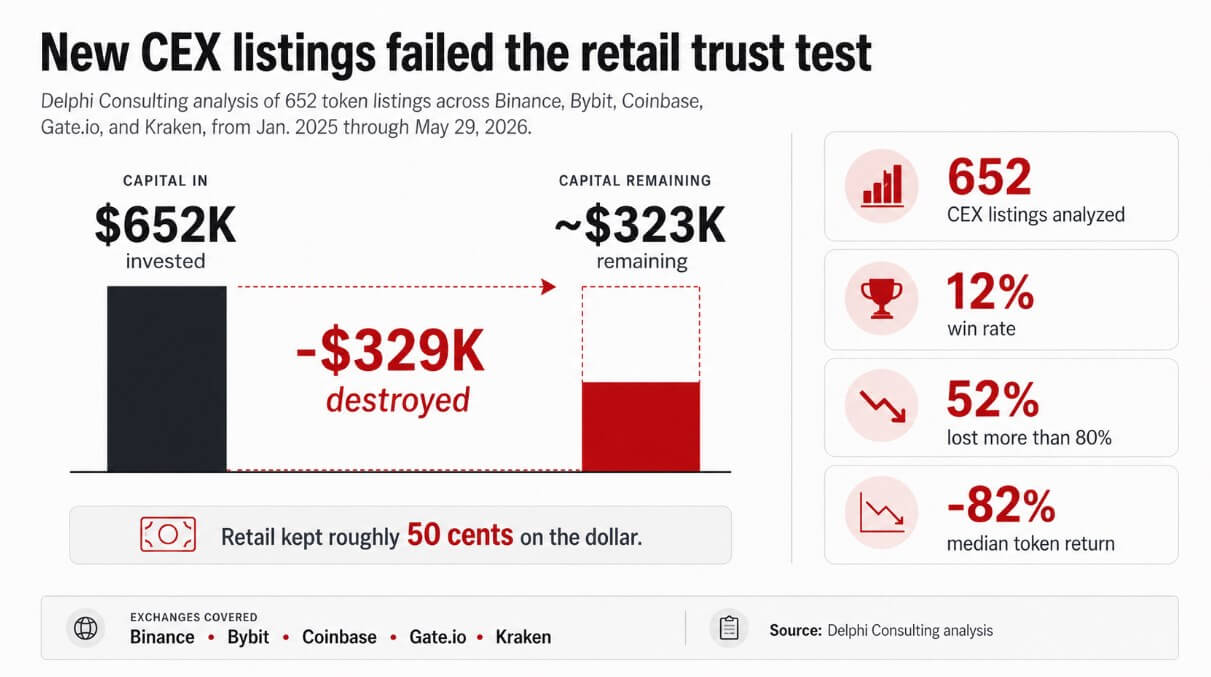

A Delphi Consulting evaluation of 652 CEX listings from January 2025 onward discovered {that a} consumer shopping for each new token throughout Binance, Bybit, Coinbase, Gate.io, and Kraken would have stored roughly 50 cents on the greenback.

The win fee throughout all listings was 12%, 52% of tokens misplaced greater than 80%, and the median return was -82%. Tokenized shares look like the reply that exchanges are giving to failing token launches.

Kraken now affords greater than 100 tokenized shares and ETFs by its xStocks product, with 24/5 buying and selling, $1 minimums, and self-custody help.

Robinhood EU lists greater than 2,000 Inventory Tokens linked to Nvidia, Microsoft, Apple, and the Vanguard S&P 500, with minimums of €1 and 24/5 entry.

Coinbase affords inventory and ETF buying and selling inside the identical app as crypto, with zero fee, USDC funding, and $1 fractional shares for US customers, with a longer-term plan to make tokenized shares obtainable globally as on-chain collateral.

Tokenized shares throughout all platforms held $1.48 billion in distributed worth as of June 1, up 39% over 30 days, with $4.2 billion in month-to-month switch quantity.

What Binance Analysis says the chance is

Binance Analysis reported that fairness possession exterior the US runs broadly beneath 20%, in contrast with 62% of People holding equities, attributing the hole to infrastructure entry.

The identical report initiatives that crypto exchanges might channel $2 trillion in incremental capital and practically 300 million new customers into world fairness markets by 2031 beneath a base case, rising to $5 trillion in annual incremental fairness capital beneath a bull case.

Some AI-cycle shares traded above $1,000 per share in periods when common month-to-month wages in components of Africa and Southern Asia have been beneath $300, making single-share possession inaccessible with out fractional shares.

Binance says stablecoins might take away a median of three.6% and about $40 per transaction in cross-border off-ramp prices, and that TradFi-linked perpetuals already account for roughly 10% of stablecoin buying and selling quantity, positioning stablecoins as general-market entry infrastructure.

| Binance Analysis level | Why it issues for tokenized shares |

|---|---|

| Fairness possession exterior the US broadly beneath 20% vs 62% within the US | Massive entry hole for emerging-market customers |

| Almost 300M potential new customers by 2031 | Crypto exchanges develop into world brokerage gateways |

| $2T base-case incremental capital by 2031 | Tokenized equities develop into a serious monetary entry product |

| $5T bull-case annual incremental fairness capital | Upside case if crypto rails develop into normalized fairness infrastructure |

| Stablecoins can cut back off-ramp prices by 3.6% / ~$40 per transaction | Stablecoins develop into brokerage money, not simply crypto buying and selling collateral |

| TradFi-linked perps at ~10% of stablecoin buying and selling quantity | Demand for non-crypto belongings is already showing inside crypto markets |

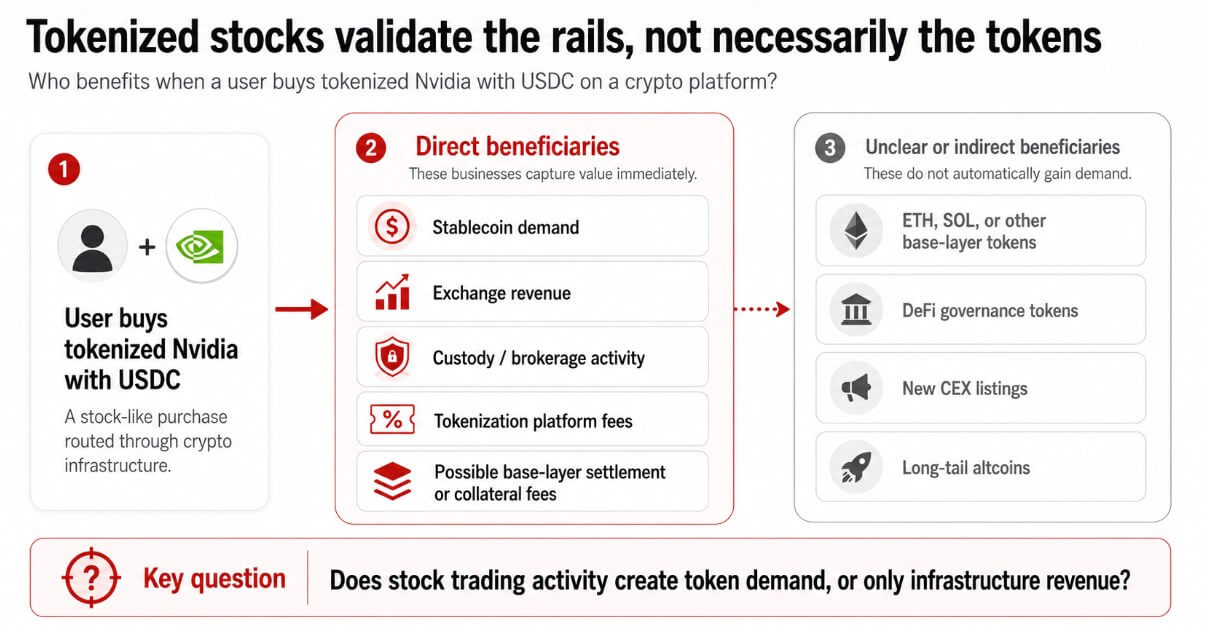

A consumer shopping for tokenized Nvidia with USDC creates demand for stablecoin settlement, change income, custody exercise, and tokenization platform charges.

If inventory buying and selling exercise routes by base-layer networks for settlement or collateral, choose protocols might seize price and staking demand from fairness flows that by no means contact a brand new token itemizing, increasing the full addressable market even when crypto asset adoption stagnates.

The Delphi information and what it says about demand

Numbers from a latest Delphi report present that exchanges spent the 2025 cycle itemizing a whole lot of tokens that overwhelmingly destroyed retail capital, and the identical platforms now providing Nvidia or Apple publicity are implicitly conceding that the native itemizing product misplaced consumer belief.

A retail consumer with a stablecoin steadiness can now purchase tokenized publicity to an organization with quarterly earnings, analyst protection, and a well-recognized model by the identical account that beforehand supplied solely new token listings at a -82% median return.

Tokenized shares give current crypto account holders a competing asset class inside the identical account, and if exchanges achieve making that the first progress product, they validate crypto rails whereas lowering the addressable demand pool for brand spanking new token listings.

Institutional allocators rotating from Bitcoin ETFs into AI equities, and retail customers in crypto apps selecting tokenized shares over new listings, put the structural demand argument for long-tail tokens beneath simultaneous strain from each ends of the capital stack.

Exchanges operating that mannequin develop into TradFi distributors on crypto infrastructure, capturing inventory buying and selling income whereas the native itemizing enterprise shrinks to a secondary product.

Base layers should still profit from settlement and collateral exercise, however governance tokens, new altcoin listings, and belongings with out earnings or utility face a valuation downside that tokenized shares make tougher to disregard.

What the merchandise truly are

Kraken says xStocks present value publicity with out shareholder rights equivalent to voting, and Robinhood describes its Inventory Tokens as by-product contracts that carry liquidity, forex, and counterparty dangers.

The SEC warns that third-party and artificial tokenized securities might not characterize possession of or contractual obligations tied to the underlying safety, exposing holders to the danger of issuer or custodian chapter.

Tokenized shares might cut back friction and develop attain, however customers in rising markets shopping for stock-like publicity by a crypto change might uncover throughout a market-stress occasion that they’ve held an artificial product.

The infrastructure win and the possession disconnect can coexist, and it issues most exactly when market situations make it most related.

The place worth truly accrues

Stablecoins, exchanges, custodians, and tokenization issuers seize worth from tokenized inventory exercise no matter whether or not crypto-native tokens profit.

A consumer funding a tokenized Nvidia buy with USDC by Kraken generates stablecoin demand, change income, and tokenization platform charges with out producing demand for ETH, SOL, or any new altcoin itemizing.

The bull case for crypto tokens requires that inventory buying and selling exercise creates collateral, settlement, or staking demand that flows by crypto-native belongings.

That chain of worth seize is commercially believable however relies on product design decisions that exchanges haven’t but totally dedicated to.

Binance Analysis’s $2 trillion base case and $5 trillion bull case describe capital flowing by crypto infrastructure with out essentially creating demand for crypto-native tokens, which depend upon separate design decisions that exchanges haven’t but dedicated to.

{kind=link}